| Map

> Data Science > Predicting the Future >

Modeling >

Classification > Logistic Regression |

|

|

|

|

|

|

Logistic

Regression

|

|

|

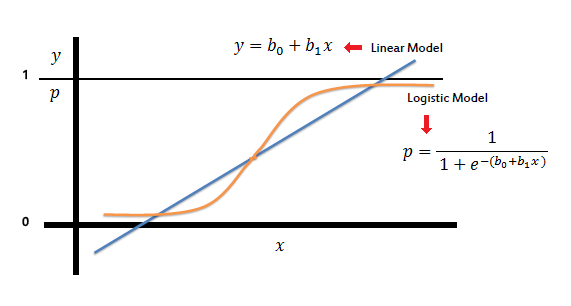

| Logistic regression predicts the probability of an

outcome that can only have two values (i.e. a dichotomy). The prediction is based on the use of one or several predictors

(numerical and categorical). A linear regression is not appropriate for predicting the value of a binary variable for two reasons: |

|

|

|

|

|

- A linear regression will predict values outside

the acceptable range (e.g. predicting probabilities

outside the range 0 to 1)

- Since the dichotomous experiments can only have

one of two possible values for each experiment, the residuals will not

be normally distributed about the predicted line.

|

|

|

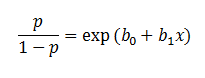

| On the other hand, a logistic regression produces a logistic

curve, which is limited to values between 0 and 1. Logistic regression is

similar to a linear regression, but the curve is constructed using the

natural logarithm of the “odds” of the target variable, rather than

the probability. Moreover, the predictors do not have to be normally

distributed or have equal variance in each group. |

|

|

|

|

|

|

| In the logistic regression the constant (b0)

moves the curve left and right and the slope (b1)

defines the steepness of the curve. By simple transformation, the logistic regression equation can be written in terms of an odds ratio. |

|

|

|

|

|

|

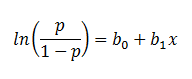

| Finally, taking the natural log of both sides, we can write the equation in terms of

log-odds (logit) which is a linear function of the predictors. The coefficient (b1)

is the amount the logit (log-odds) changes with a one unit change in x. |

|

|

|

|

|

|

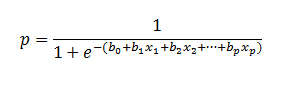

| As mentioned before, logistic

regression can handle any number of numerical and/or categorical variables. |

|

|

|

|

|

|

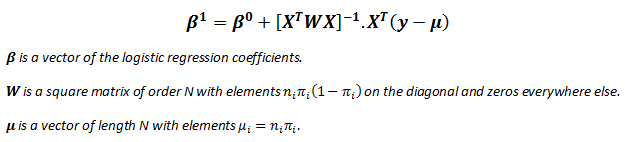

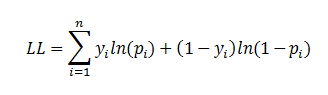

| There are several analogies between linear regression and logistic regression. Just as

ordinary least square regression is the method used to estimate coefficients for the best fit line in linear regression, logistic regression

uses maximum likelihood estimation (MLE) to obtain the model coefficients that relate

predictors to the target. After this initial function is estimated, the process is repeated until LL (Log Likelihood) does not change significantly. |

|

|

| |

|

|

|

|

|

|

| |

|

|

| A pseudo R2 value is also available to indicate

the adequacy of the regression model. Likelihood ratio test is a test of the significance of the difference between the likelihood ratio for the baseline model minus the likelihood ratio for a reduced model.

This difference is called "model chi-square“. Wald test

is used to test the statistical significance of each coefficient (b) in the

model (i.e., predictors contribution).

|

|

|

| |

|

|

| Pseudo R2

|

|

|

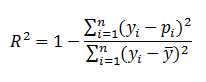

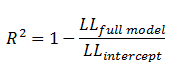

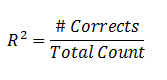

| There are several measures intended to mimic the R2

analysis to evaluate the goodness-of-fit of logistic

models, but they cannot be interpreted as one would interpret an

R2 and different pseudo R2 can arrive at very different values.

Here we discuss three pseudo R2measures. |

|

|

| |

|

|

|

Pseudo R2 |

Equation |

Description |

|

Efron's |

|

'p' is the

logistic model predicted probability. The model residuals are squared, summed, and divided by the total variability in the dependent variable. |

|

McFadden's |

|

The ratio of the log-likelihoods suggests the level of improvement over the intercept model offered by the full model. |

|

Count |

|

The number of records correctly predicted, given

a cutoff point of .5 divided by the total count of cases. This is

equal to the accuracy of a

classification model. |

|

|

|

| |

|

|

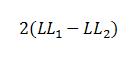

| Likelihood Ratio Test |

|

|

| The likelihood ratio test provides the means for comparing the likelihood of the data under one

model (e.g., full model) against the likelihood of the data under another, more restricted

model (e.g., intercept model).

|

|

|

|

|

|

|

where 'p'

is the logistic model predicted probability. The next step is to calculate the difference between these two

log-likelihoods. |

|

|

|

|

|

|

| The difference between two likelihoods is multiplied by a factor of 2

in order to be assessed for statistical significance using standard significance

levels (Chi2 test). The degrees of freedom for the test will

equal the difference in the number of parameters being estimated under the

models (e.g., full and intercept). |

|

|

| |

|

|

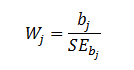

| Wald test |

|

|

| A Wald test is used to evaluate the statistical significance of each coefficient

(b) in the model. |

|

|

|

|

|

|

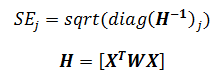

| where W

is the Wald's statistic with a normal distribution (like Z-test), b is

the coefficient and SE is its standard

error. The W value is then squared, yielding a Wald statistic with a chi-square distribution. |

|

|

| |

|

|

|

|

|

|

| |

|

|

| Predictors Contributions |

|

|

| The Wald test is usually used to assess the significance of prediction of each predictor.

Another indicator of contribution of a predictor is exp(b)

or odds-ratio of coefficient which is the amount the logit (log-odds) changes, with a one unit change in

the predictor (x). |

|

|

| |

|

|

|

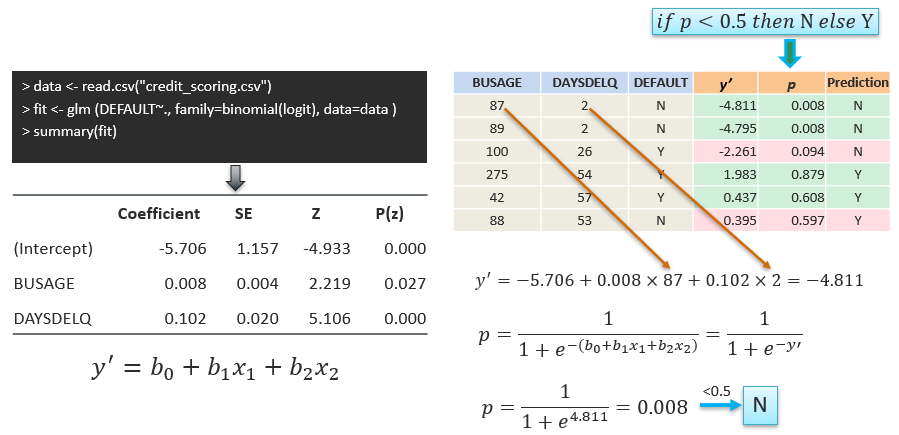

Example using R |

|

|

|

|

|

|

| |

|

|

| |

|

|

| Interpretation of Coefficients |

|

|

| Increasing BUSAGE by 1 month (and

keeping all other variables fixed) multiplies the estimated odds of DEFAULT

by exp(0.008) ≈ 1.008, or in other words, increases the odds by 0.8%. |

|

|

| Increasing DAYSDELQ by 1 day (and

keeping all other variables fixed) multiplies the estimated odds of DEFAULT

by exp(0.102) ≈ 1.07, or in other words, increases the odds by 7%. |

|

|

| |

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

|